An important concept to understand is that public real estate investment trusts (REITs) transact at a market price that is usually above or below the value of the underlying investments.

In comparison, private real estate funds transact at value. Investors typically buy into and redeem out of the funds at net asset value (NAV), which is driven largely by the appraised value of the underlying assets of the funds.

Real estate interval funds, like the Versus Capital Multi-Manager Real Estate Income Fund (“VCMIX”, the “Fund”), which allow daily purchases and offer periodic repurchase offers, tend to sit in the middle. VCMIX typically targets an approximate 25% allocation to public real estate securities (including REITs) and 75% allocation to private real estate funds. Transactions occur at the Fund’s NAV, which is calculated daily1.

While there are myriad reasons to invest in public REITs or private real estate, there are less-understood frictional “costs” associated with each asset class. This blog will attempt to explain these costs which we believe are important to understand before investing in either public or private real estate.

Transacting at Price vs. Value

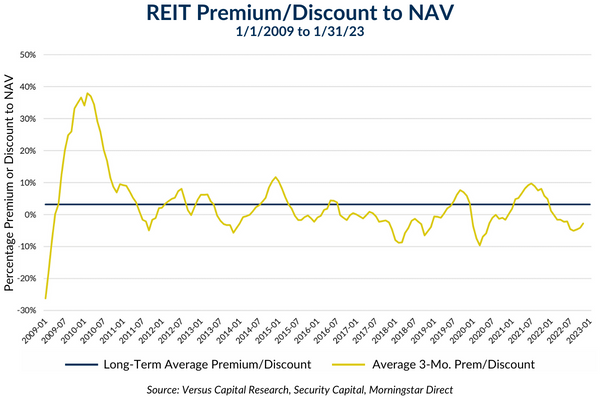

There are typically periods during an economic cycle where real estate faces one headwind or another. Beginning around the start of 2022, REITs encountered a headwind in the form of higher interest rates which increased the cost of capital for real estate operations. Market perception of this change drove the price of REITs down more quickly than the actual impacts to real estate value. As a result, REITs traded at a discount for most of 2022.

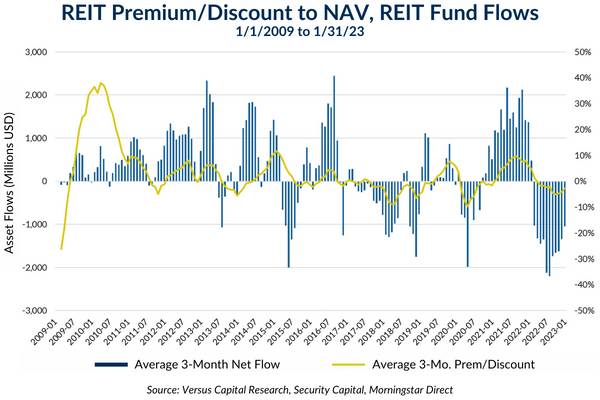

The idea of buying REITs at a discount and waiting for the price to revert to the mean may seem like a tempting proposition since REITs have averaged a 3% premium to NAV over the long term, as shown on the chart above. However, investors in REIT-focused mutual funds and ETFs have not historically been good at taking advantage of discounted valuations, as illustrated by fund flows, below.

The blue bars in the above chart represent domestic REIT mutual fund and exchange-traded fund (ETF) flows. Rather than buying REITs when they are trading at a discount to NAV, investors instead tend to pile into the asset class when REITs have performed well and are trading at a premium, paying more for the security than the value of the investments it represents. The same can be seen on the downside – investors tend to exit REITs when they are trading at a discount to NAV.

If an investor sells a REIT when the security is trading at a 10% discount to NAV, he or she is effectively getting back 90 cents on the dollar relative to the underlying value of the real estate. This is a frictional “cost” of daily liquidity. In other words, REIT investors may (and often do, as seen by the flow data above) accept a price significantly less than the value of the real estate to receive immediate liquidity.

During periods of market uncertainty, managers of private real estate funds may need to restrict liquidity, also known as “prorating” redemptions, given the relatively illiquid nature of private commercial real estate. However, during these periods of proration when investors are only receiving a portion of their redemption request, they are still transacting at NAV rather than receiving a discounted price.

Funds in proration are essentially telling their investors the fund can only redeem a portion of fund shares at 100% of their value. So, the frictional “cost” of limited liquidity investing is investors may not receive all their requested liquidity during a redemption period, but they do receive full value for their shares.

We believe investors are well-served by understanding these frictional costs as well as volatility differences and their own behavioral tendencies when considering how to allocate to real estate. We believe the lower volatility of private core real estate buffers investors against the illiquidity risk and pitfalls of market timing while still providing the potential for attractive risk-adjusted returns.

Whether investing in public REITs or private real estate, we are strong advocates of holding for the long-term, ideally across multiple market cycles, in order to capture the strong upside that real estate investments (on average) have historically provided.

If you are not already subscribed to our insights, we invite you to fill out the form below to be notified when we release new information on real assets investing.

DISCLOSURES:

1While VCMIX strikes a daily NAV, most of its underlying private funds publish a quarterly NAV. As such, VCMIX fair values these investments in the interim periods. For more information on the Fund and its valuation policies and procedures, please see the Fund’s prospectus.

INVESTORS SHOULD CAREFULLY CONSIDER THE FUND’S INVESTMENT OBJECTIVES, RISKS, CHARGES, AND EXPENSES BEFORE INVESTING. A PROSPECTUS WITH THIS AND OTHER INFORMATION ABOUT THE FUND MAY BE OBTAINED FROM THE VERSUS CAPITAL WEB SITE (versuscapital.com). INVESTORS SHOULD READ IT CAREFULLY BEFORE INVESTING. AN INVESTMENT IN THE FUND IS SUBJECT TO A HIGH DEGREE OF RISK. THESE RISKS INCLUDE, BUT ARE NOT LIMITED TO, THOSE OUTLINED BELOW.

- Real estate entails special risks, including tenant default, environmental problems, and adverse changes in local economies. Additionally, the capital value of the Fund’s investments may be significantly diminished in the event of a downward turn in real estate market prices.

- Defaults among mortgage loans in which the Fund invests may result in the Fund being unable to repossess and sell the underlying properties in a timely manner. The resulting time delay could reduce the value of the investment in the defaulted mortgage loans.

- The Fund is "non-diversified" under the Investment Company Act of 1940. Changes in the market value of a single holding may cause greater fluctuation in the Fund's net asset value than in a "diversified" fund. The Fund is not intended as a complete investment program but instead as a way to help investors diversify into real estate. Diversification does not ensure a profit or guarantee against a loss.

- A multi-manager strategy involves certain risks. For example, it is possible that some Private Fund managers may take similar market positions, thereby interfering with the Fund’s investment goal. The Fund may borrow as an investment strategy, up to one third of the Fund’s gross asset value. Borrowing presents opportunities to increase the Fund’s return, but potentially increases the losses as well. Because the Private Funds may themselves borrow and incur a higher level of leverage than that which the Fund is permitted, the Fund could be effectively leveraged in an amount far greater than the limit imposed by the Investment Company Act of 1940.

- The adviser, sub-advisers and Private Fund managers manage portfolios for themselves and other clients. A conflict of interest between the Fund and these other parties may arise which could disadvantage the Fund. For example, a suitable but limited investment opportunity might be allocated to another client rather than to the Fund.

- The Fund's investments in Private Funds are priced based on estimates of fair value, which may prove to be inaccurate. Therefore, the value of the Fund's investments will be difficult to ascertain, and the valuations provided in respect of the Fund's Private Funds and other private securities, will likely vary from the amounts the Fund would receive upon withdrawal of its investments. Additionally, given the limited liquidity of the Private Funds, the Fund may not be able to alter its portfolio allocation in sufficient time to respond to any underlying material changes, resulting in substantial losses from risks of Private Funds.

- Fund holdings and sector allocations are subject to change at any time and should not be considered recommendations to buy or sell any security.

- The Fund does not intend to list its shares on any securities exchange during the offering period, and a secondary market in the shares is not expected to develop. There is no guarantee that shareholders will be able to sell all of their tendered shares during a quarterly repurchase offer. An investment is not suitable for investors that require liquidity, other than through the Fund’s repurchase policy.

- You should not expect to be able to sell your shares other than through the Fund’s repurchase policy, regardless of how the Fund performs.